Buying a House in the Netherlands: A Complete Guide

(Including Mortgages & Renovations!)

Buying a house in the Netherlands can feel like an emotional rollercoaster—exciting, stressful, and a little overwhelming all at once. Whether you’re an expat, a first-time buyer, or purchasing your second home, this guide will walk you through the process step by step, from understanding Dutch mortgages to navigating government incentives and even renovating your new home. Let’s turn that dream home into reality! 🏡

Why Buy Instead of Rent?

Renting in the Netherlands can be expensive, with limited availability in major cities. Here’s why buying might be a smarter move:

✔ Lower Monthly Costs: Mortgage payments can often be cheaper than rent.

✔ Build Equity: Instead of paying rent to a landlord, you’re investing in your own property.

✔ Tax Benefits: Mortgage interest can be tax-deductible.

✔ Stability: No sudden rent hikes or unexpected evictions.

Sounds great, right? But first, let’s understand the steps to buying a home in the Netherlands.

Step-by-Step Guide to Buying a House

Step 2: House Hunting & Making an Offer

🏠 Where to search for houses?

Funda.nl (largest real estate platform)

Local real estate agents (makelaar)

Expat-focused property websites

🔑 Tips for a strong offer:

Houses often sell for above asking price in major cities.

Have your mortgage pre-approval ready.

Be quick! The Dutch housing market moves fast.

🔹 Want to check historical home prices in your area? Visit Kadaster Housing Data to see past home purchases by postcode!

📈 Will house prices rise or fall? ABN AMRO predicts Dutch house prices will increase by 7% in 2025 and 3% in 2026. Every year, major banks publish housing market forecasts, which can help buyers time their purchases strategically. 🔗 Read the latest ABN AMRO Housing Market Report

Step 1: Check Your Budget & Get a Mortgage Pre-Approval

💰 Determine how much you can borrow with an online mortgage calculator or by consulting a mortgage adviser (Hypotheekadviseur). They help you compare lenders and navigate complex mortgage terms. While their services aren’t free, they can save you money in the long run by finding the best deals.

✅ Pros of Hiring a Mortgage Adviser:

Access to better mortgage rates

Guidance on government incentives and tax deductions

Help with paperwork and Dutch financial jargon

❌ Cons:

Fees can be expensive (typically €2,000–€3,000)

Not always necessary if you have simple finances

If you prefer a DIY approach, you can go directly to banks like Rabobank, ING, or ABN AMRO.

🔹 Need a free consultation? You can schedule a free call with a mortgage advisor here: Easy Mortgage Free Call

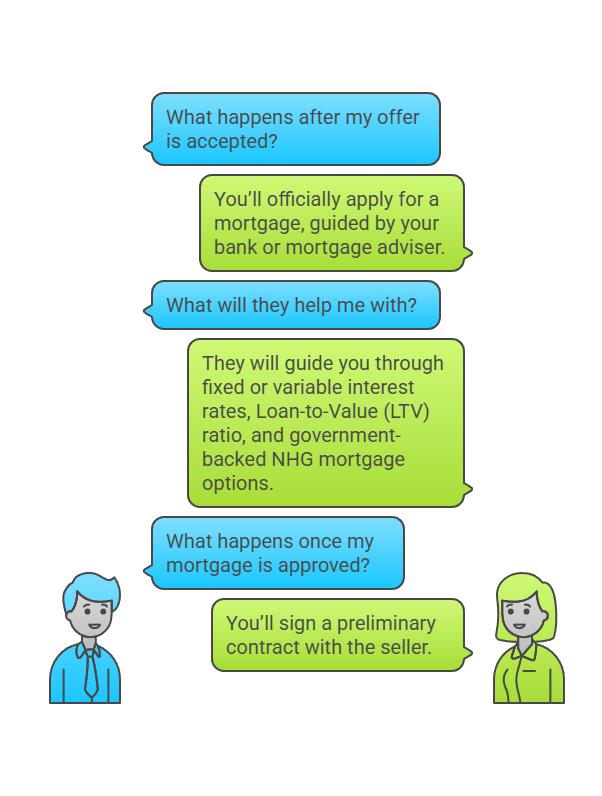

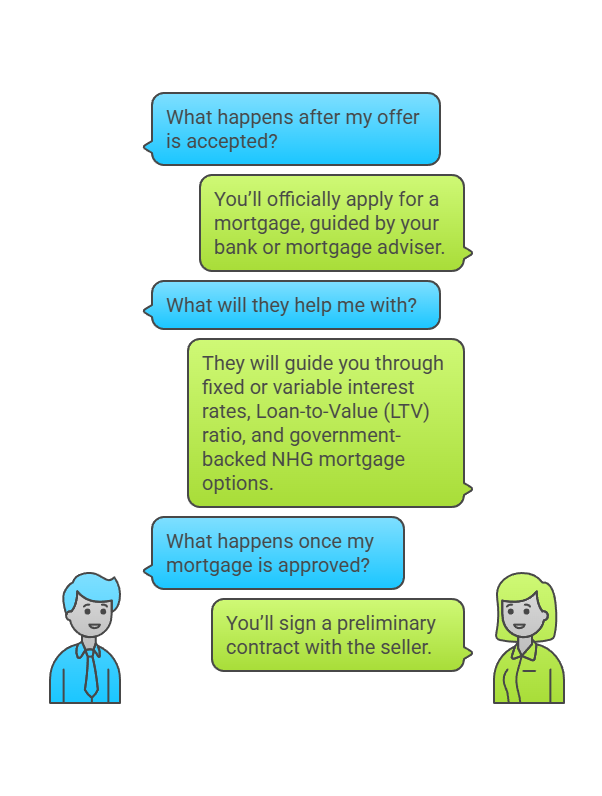

Step 3: Getting Your Mortgage & Signing Contracts

🏦 After your offer is accepted, you’ll officially apply for a mortgage (hypotheek). Your bank or mortgage adviser will guide you through:

Fixed or variable interest rates

Loan-to-Value (LTV) ratio

Government-backed NHG mortgage (lowers risk & interest rates)

Once approved, you’ll sign a preliminary contract (koopakte) with the seller.

🔹 Did you know? Your mortgage amount may vary based on your home's energy label. More efficient homes often qualify for better loans. Check options here: SVN Starterslening

Bouwdepot: Financing Renovations with Your Mortgage

If you’re buying a house that needs renovations, you might need a bouwdepot. This is a renovation loan that’s included in your mortgage, allowing you to finance home improvements like:

✔ New kitchen or bathroom

✔ Insulation or solar panels

✔ Expanding living space

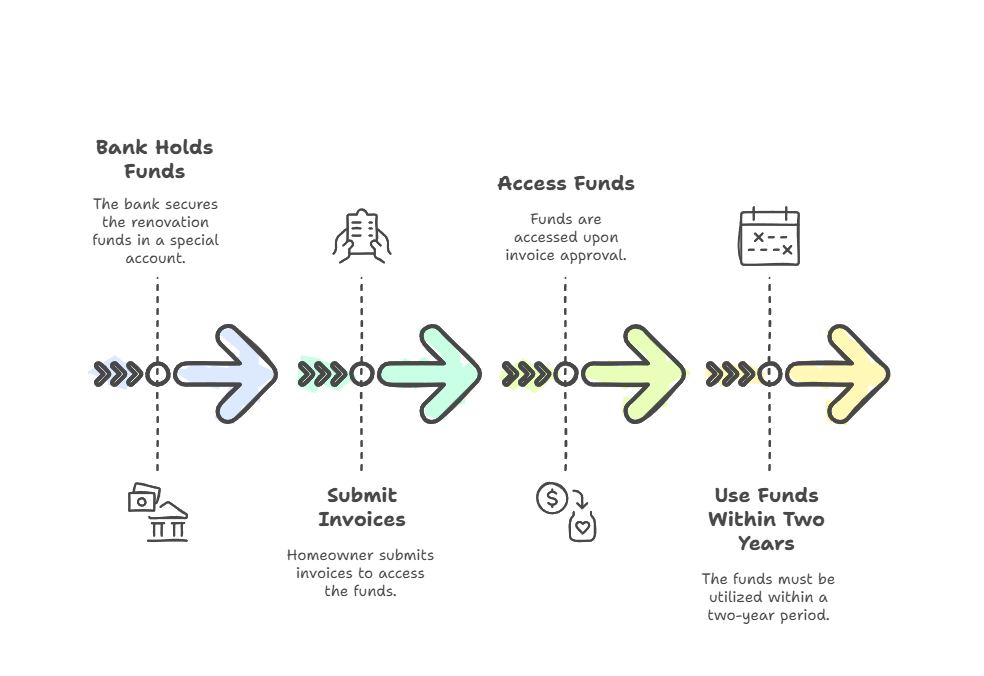

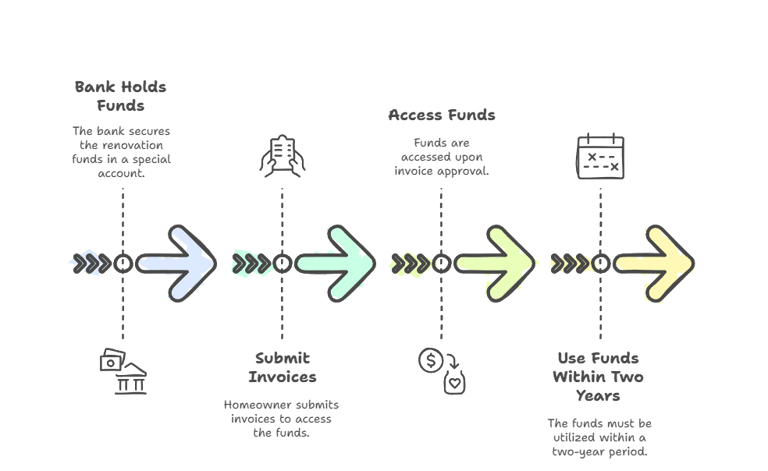

How Does Bouwdepot Work?

The bank holds the renovation funds in a special account.

You submit invoices to access the money.

The funds must be used within two years.

🔹 Pro Tip: Renovation costs are often tax-deductible! Keep all invoices for your tax return.

🏡 The Dutch government offers financial assistance to homeowners, including:

NHG Mortgage (Nationale Hypotheek Garantie): Reduces interest rates and provides safety in case of financial difficulties.

Starterslening (First-time Buyer Loan): Extra financing for new buyers.

Energy Subsidies: Grants for installing solar panels, insulation, and heat pumps.

Transfer Tax Exemption: First-time buyers under 35 don’t pay the 2% property transfer tax (if the house costs less than €440,000).

📌 Check your local municipality’s website for specific subsidies!

Government Incentives & Subsidies

Common Mistakes to Avoid

Life After Buying: Renovation, Insurance & Taxes

🎭 Did you know that Dutch real estate agents often host open house days where anyone can view multiple houses without making an appointment?

🏠 Some historic Dutch homes have hooks at the top for lifting furniture in through windows—because the staircases are too narrow!

💡 The Netherlands has one of the highest rates of homeownership in Europe, but buying a home here takes an average of 3–6 months from start to finish!

📜 Dutch mortgages can last up to 30 years, but many people pay them off early to save on interest.

Buying a home in the Netherlands is a big step, but with careful planning and the right knowledge, it can be a rewarding investment. Whether you're looking for stability, lower housing costs, or a long-term financial gain, understanding the mortgage process and available incentives will help you make informed decisions. Be sure to work with trusted professionals, budget for extra costs, and explore renovation options to make the most of your new home. Happy house hunting! 🏡

Got questions? Drop them in the contact form!

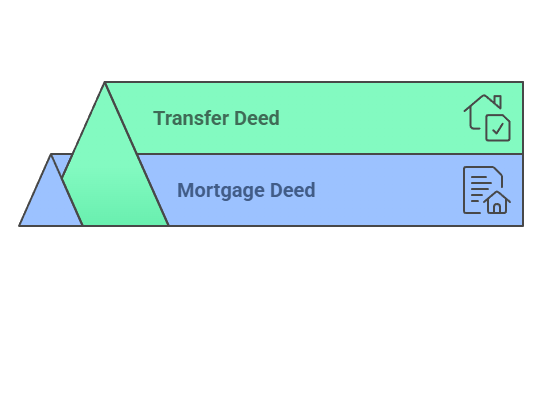

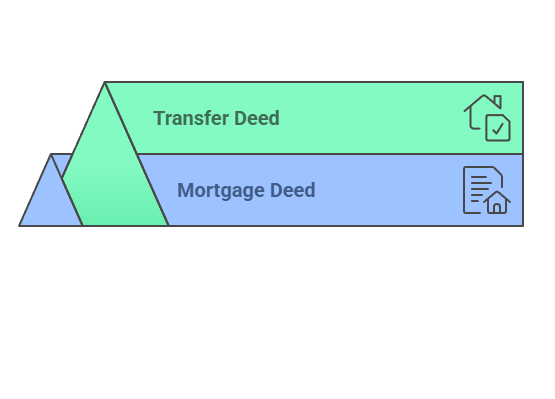

Step 4: The Notary & Official Transfer

📜 In the Netherlands, a notary (notaris) is required to finalize the property purchase. You’ll sign two key documents:

The Mortgage Deed – Confirms your loan.

The Transfer Deed – Makes you the official homeowner!

Congratulations, you now own a Dutch home! 🎉

❌ Not budgeting for extra costs:

Notary fees (€1,000–€2,000)

Real estate agent commission (1–2%)

Property transfer tax (2%, unless exempt)

❌ Skipping a house inspection:

Older Dutch homes might have hidden issues like foundation problems.

❌ Underestimating renovation costs:

Always get multiple quotes for renovations.

Renovating Your New Home

Renovating in the Netherlands takes patience! Expect long waiting times for contractors. Popular home improvement projects include:

🔨 Adding extra rooms or expanding the living space

🔨 Upgrading insulation to reduce energy bills

🔨 Installing solar panels (subsidies available!)

Home Insurance & Property Taxes

Don’t forget:

🏡 Home insurance (woonverzekering) – Required for a mortgage.

🏡 Municipal taxes (gemeentelijke belastingen) – Includes waste disposal & water tax.

🏡 Annual property tax (onroerendezaakbelasting) – Based on your home’s value.

Fun Facts About Buying a House in the Netherlands

NetherGuides

Your resource for thriving in the Netherlands.

© 2024. All rights reserved.

Top 10 Things to Do When You Arrive in the Netherlands

Daycare, Schools, and Activities in the Netherlands

How to Open a Bank Account in the Netherlands

Residence Types and Registration Process

Housing types and finding a home

Dutch Higher Education

Health Insurance in the Netherlands

Work Permits and Rights in the Netherlands

Essentials for Everyday Life in the Netherlands

Quick Facts and FAQ